The closing entry is used in accounting to set the balance for temporary accounts (drawing, expense and revenue accounts) to zero at the end of an accounting period. Other accounts such as the liability, retained earnings, and asset accounts are kept open because they are permanent accounts. The balances for these accounts are carried over to the next accounting period without resetting them to zero.

Closing Entries Video Tutorial With Examples

The closing entries are performed for temporary accounts so that their balance is zero in preparation for the next accounting period. The balance for the temporary accounts will be shown in the company’s retained earnings capital account after the closing entries are completed.

Closing Entries Video Example 1

Closing Entries Video Example 2

Step 1 – Record the Revenue to Income Summary Closing Entry

The revenue account shows the company’s total review for the accounting period. The balance for the revenue is recorded in the income summary for the company, since revenue is one of the parts of income calculation. The closing entry may be described as follows:

Therefore the revenue account is reset to zero while the income summary account receives a credit that is equal to the revenue balance. The revenue account can now record the revenue for the new accounting period to portray the accurate revenue for the period.

Step 2 – Record the Expenses to Income Summary Closing Entry

The second step is to record the expenses balance to the income summary account. The expenses are also used to calculate revenue, which is why they are recorded as a debit in the income summary account. The entry is usually made as follows:

Now the income summary account displays both the revenue and the expenses. The revenue is listed as a credit to the income summary account while the expenses are listed as a debit. The balance for the income summary account is now the company’s income for the accounting period. Also, the expenses account is reset to zero and is now ready to record new expense entries.

Step 3 – Close the Income Summary Account to the Company’s Retained Earnings Capital Account

Now the company’s income for the period is known, it can be closed to the retained earnings account. The retained earnings account is the company’s capital account that accumulates the income from each accounting period. This account is ongoing while the income summary account is temporary.

The entry may be described as follows:

The retained earnings account is used by the company to retain a portion of its net income for investment, security, debt payments, and on other areas of growth for the company. The retained earnings balance can be negative if the company’s income summary balance for the period is negative, and the negative income summary balance ends up being larger than the current retained earnings balance. This results in a company deficit, which means that the company has no reserve cash to use to pay towards liabilities.

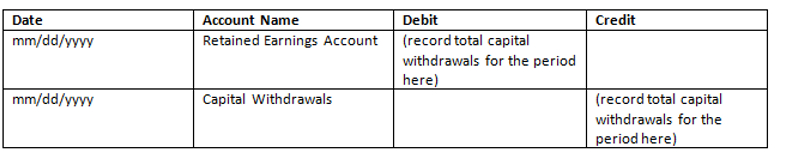

Step 4– Close Capital Withdrawals to Retained Earnings

The final step is to record any capital withdrawals (such as dividends paid to equity holders) that occurred during the account period. The capital withdrawals account should already be debited for the total amount of withdrawals that occurred during the period, so in this case the account is credited while the retained earnings account is debited.

This results in the retained earnings account showing an accurate representation of the company’s reserves. Also, this is another opportunity for a negative balance to occur on the retained earnings account. Even if a company has a positive income for the period, dividends paid at the end of an accounting period or quarter to investors can result in a deficit. As a result, some companies may withhold dividends to their equity holders if they are in financial difficulty.

Other Steps Involved in a Company’s Closing Procedure

The steps above describe a basic account closing process for a company, however this process is usually performed with software. There are other important steps that an accountant or owner will perform such as preparing and releasing financial statements, calculating quarterly income taxes and paying them, double checking the asset and liability account balances, checking the accounting for any errors, counting and valuing physical inventory, calculating sales commissions and much more.

Every company will have its own unique closing procedure depending on the type of business it is, and many companies have complicated closings that require the effort of several accountants. Also, companies that happen to use subledgers usually close them out each period before they can close out the general ledger, which can add more time to the process.

Although millions of people visit Brandon's blog each month, his path to success was not easy. Go here to read his incredible story, "From Disabled and $500k in Debt to a Pro Blogger with 5 Million Monthly Visitors." If you want to send Brandon a quick message, then visit his contact page here.