When a company issues just one type of stock it is called common stock, and it includes the equity shares that the owners of a company receive. Common stockholders in a company usually receive returns on their investment in the form of dividends, they usually receive a portion of the assets at the time of sale, and have significant decision making power in the company such as the ability to vote on the board of directors.

Common Stock Journal Entry Video Tutorial With Examples

Companies regularly sell their common stock in exchange for investment capital. The investor receives common shares of the company and becomes an owner of the company as well. There are three major types of stock transactions including repurchasing common stock, selling common stock, and exchanging stock for non-cash assets and services.

The accounting for each type of transaction is different. The cash sale of stock depends on the par value, or the capital per stock share. The par value of a stock is shown on the front of the certificate, and in many cases the par value of a stock is set at $0.01 per share, or not may have no par value at all.

Companies do this to protect their shareholders from liability. For instance, if the company’s par value of a stock is at $8 per share, but the price of the stock falls to $4 per share, the shareholders are liable for $4 per share if the stocks are redeemed at their par value. The par value of a stock has no relationship to the price at which it is traded; investors will pay whatever they feel the stock is worth at the time.

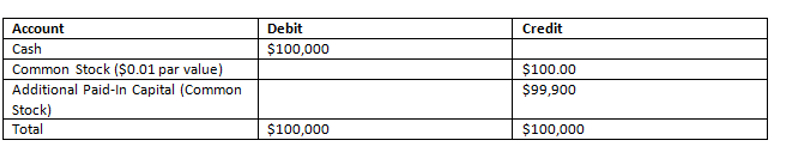

Selling common stock for cash is the most common scenario. It is recorded with a credit in the common stock account with the par value listed for each share. Another entry is made in the cash account for the amount of cash received. There is also an entry for additional paid-in capital, which is a credit for the amounts in excess of the par value that investors paid for the stock.

Common Stock Journal Example

In the following example, ABC Advertising sells 10,000 shares of its common stock at $10 per share. The sale is recorded as follows:

When the sale has been recorded, both total columns should match. The common stock row shows the total par value of the stock that is sold. The par value plus the additional-paid in capital amount should always equal the debit to the cash account. In the rare case that the company sold the stock for its par value, there would be no additional paid-in capital entry to the common stock account.

If ABC Advertising sold preferred stock instead of common stock, the only difference would be to change the label for the Common Stock row to Preferred Stock.

Stock Repurchase Journal Example

Another circumstance that commonly arises is the repurchase of stock. This occurs when the board of directors of a company repurchases stock to reduce the amount of available stock on the market, and this stock is known as treasury stock.

When treasury stock is purchased by the board of directors, it is listed as a debit to the treasury stock account and a credit to the cash account.

For example if ABC Advertising decides to repurchase 900 shares of its common stock at $10 per share, the entry may look like the following:

A $9,000 credit is reported to the cash account, as the company has paid back some of the cash that it has received from investors, while $9,000 is debited to the treasury stock account. If the stocks are sold in the future at a price that is higher than the repurchase price, the extra amounts from the sale are recorded in the additional paid-in capital account.

If the stock is later sold at a lower amount than the repurchase cost, the first account that is debited to cover the cost is the additional paid-in capital account, followed by the company’s retained earnings account.

Stock Issued for Non-Cash Assets Example

If ABC Advertising wants to issue common stock for non-cash assets, it can assign a particular value to its common stock shares based on their market value or on the value of the non-cash services or assets that are being received.

Once a value has been determined, the amount of shares sold multiplied by the value of each share is recorded as a debit in the service or asset expense account, and a credit in the additional paid-in capital account.

In this example, ABC Advertising sells 5,000 shares of its stock to manufacturing company that produces their print flyers for a year at $10 per share. The issuance of the shares is recorded similarly to the common stock journal entry:

Although millions of people visit Brandon's blog each month, his path to success was not easy. Go here to read his incredible story, "From Disabled and $500k in Debt to a Pro Blogger with 5 Million Monthly Visitors." If you want to send Brandon a quick message, then visit his contact page here.