The China semiconductor industry has been showing an upward trend in the past 10 years. The goal has been to become competitive with the semiconductor industry in Taiwan. Because of this upward push, the Chinese industry has seen triple the annual growth rate of the global industry.

Since 1999, revenues within the semiconductor industry in China have only decreased twice, the other year being 2009.

The strength of the industry comes through fabless manufacturing. These companies design microchips internally, then contract the production of the product to other factories. Because they do not perform their own fabrication, they are given the “fabless” moniker.

Data from the industry suggests that there are notable strengths and notable weaknesses that must be addressed.

Interesting China Semiconductor Industry Statistics

#1. Revenues within the fabless section of China’s semiconductor industry accounted for revenues that exceeded $20 billion for the first time. China represents one-quarter of the global fabless industry. (Pricewaterhouse Coopers LLC)

#2. From 2005-2015, the semiconductor industry in China grew with a CAGR of 18.7%. At the same time, the global semiconductor market grew with a CAGR of 4% over the same period. This is while consumption of semiconductors grew at a rate of 14.3%. (Pricewaterhouse Coopers LLC)

#3. Wafer fabrication has also been a point of emphasis within the China semiconductor industry. In 2015, the industry increased the number of fabrication plants in this segment to 169. That brought their total share of global wafer fabrication to 12.7%. (Pricewaterhouse Coopers LLC)

#4. In 2015, the total market value for the semiconductor industry in China was $215.6 billion. In 2000, the total market value was just $14.4 billion. (Pricewaterhouse Coopers LLC)

#5. In 2017, annual revenues from China’s semiconductor industry achieved $78 billion, which was a growth rate of 19.4% over the year before. In 2018, revenues are forecast to climb by 20%. Average growth in the global industry, for comparison, is just 3.4%. (Forbes)

#6. The Chinese semiconductor market accounts for 33% of the total global supply. When accounting for chips that are used in everyday products, the industry share drops to 15%. (McKinsey)

#7. Chinese companies involved in the semiconductor industry influence the design of semiconductors or elements of its fabrication in 2% or less of all finished chips. (McKinsey)

#8. Chinese companies are able to claim less than4% of the total global revenues that are possible in the segments of front-end manufacturing and semiconductor design. (McKinsey)

#9. There are two primary barriers that stop increased competition from China’s semiconductor industry: a lack of IP and overall knowledge. Several large segments of the industry are using older technologies, such as AICs and microcontrollers, which limits the positive influence the industry has globally. At the same time, however, these two “outdated” segments still contributed $60 billion in 2010. (McKinsey)

#10. Just under 30% of the semiconductors that are produced by the Chinese industry are dedicated to data processing needs. Another 29% are used for communications. Both are below global averages. (Pricewaterhouse Coopers LLC)

#11. Chinese semiconductors are used in consumer products more than 20% of the time and in medical or industrial applications about 16% of the time. These rates are about double that of the global industry average. (Pricewaterhouse Coopers LLC)

#12. The one place where China’s semiconductor industry has not had any influence is within the aerospace and military sector. The industry has a 0% application rate for their semiconductors in that sector. (Pricewaterhouse Coopers LLC)

#13. Intel, Samsung, and SK Hynix continue to be the top 3 suppliers of semiconductors to the Chinese market. Only 14 companies in total have been amongst the top 10 suppliers to the market over the past 12 years. (Pricewaterhouse Coopers LLC)

#14. Growth rates in the O-S-D sector have been the highest for the semiconductor industry in China. Since 2003, optoelectronics, sensors, and discrete devices have seen growth rates over 35% every year. Since 2003, there have been 9 years when growth rates were over 40%. (Pricewaterhouse Coopers LLC)

#15. Integrated circuit design as a segment has shown consistent increases since 2003, when it achieved a growth rate of 6.5%. In 2015, the IC design sector had a growth rate of 23.6%. Even in years when the industry declined, the IC design sector continued to show revenue growth. (Pricewaterhouse Coopers LLC)

#16. Integrated circuit design revenues in 2015 were estimated to be $21.09 billion. That was more than $4 billion more than the industry achieved in the year before. In 2000, the industry had revenues of just $130 million. (Pricewaterhouse Coopers LLC)

#17. In 2015, there was a record number of IC design enterprises operating within the semiconductor industry in China. There were 715 enterprises in total, which was 26 more than the year before. In 1990, there were just 15 enterprises. Between 2000-2002, the industry went from 98 enterprises to 389 enterprises. (Pricewaterhouse Coopers LLC)

#18. Most of the enterprises involved in the China semiconductor industry would be classified as a small business. Over 40% of the active companies employ fewer than 500 people. 50.6% of the industry is comprised of businesses that employ 100 people or less. (Pricewaterhouse Coopers LLC)

#19. The industry leads in wafer fabrication in the segments of O-S-D and dedicated foundry production, with 35% and 37% of the domestic industry respectively. In comparison, the global industry is at 18% and 24% of capacity in those segments respectively. (Pricewaterhouse Coopers LLC)

#20. China’s current wafer fab capacity is 3.3 million, which accounts for just under 14% of the global total capacity. (Pricewaterhouse Coopers LLC)

#21. The Yangtze River Delta has the largest concentration of manufacturing capabilities for the semiconductor industry. About 60% of wafer fab, testing, and packaging is located within this region, accounting for half of the total industry revenue in 2015. (Pricewaterhouse Coopers LLC)

China Semiconductor Industry Trends and Analysis

The need for semiconductors is not going away any time soon. Most of our modern electronic equipment utilizes this technology. It has become a cornerstone of modern life. The China semiconductor industry has worked hard to be an influential and competitive part of this sector, to the point where they have outpaced the growth of the global industry for multiple years in a row.

As the industry continues to evolve and mature, China looks poised to be a global leader in virtually every segment of the industry.

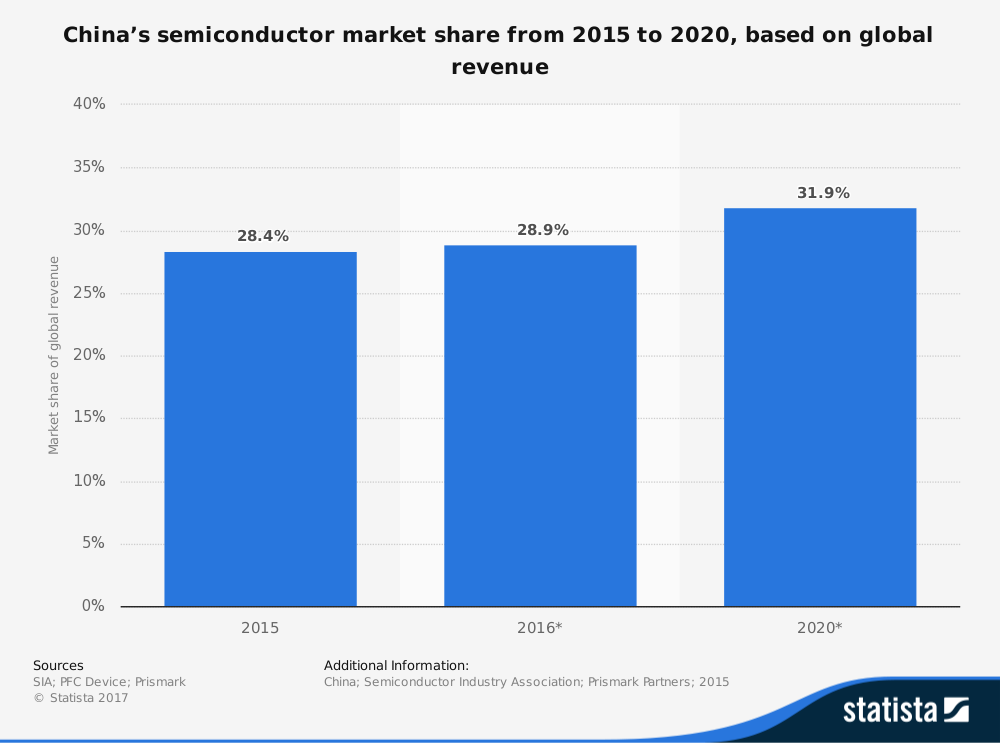

Assuming the trend of transferring global electronic equipment production to China continues and the industry can continue manufacturing productions that are above average in content, the trends seen in the last decade are expected to continue. In time, semiconductor production in China could reach up to 35% of the global need when forecast through the next decade.

Although millions of people visit Brandon's blog each month, his path to success was not easy. Go here to read his incredible story, "From Disabled and $500k in Debt to a Pro Blogger with 5 Million Monthly Visitors." If you want to send Brandon a quick message, then visit his contact page here. Brandon is currently the CEO of Aided.