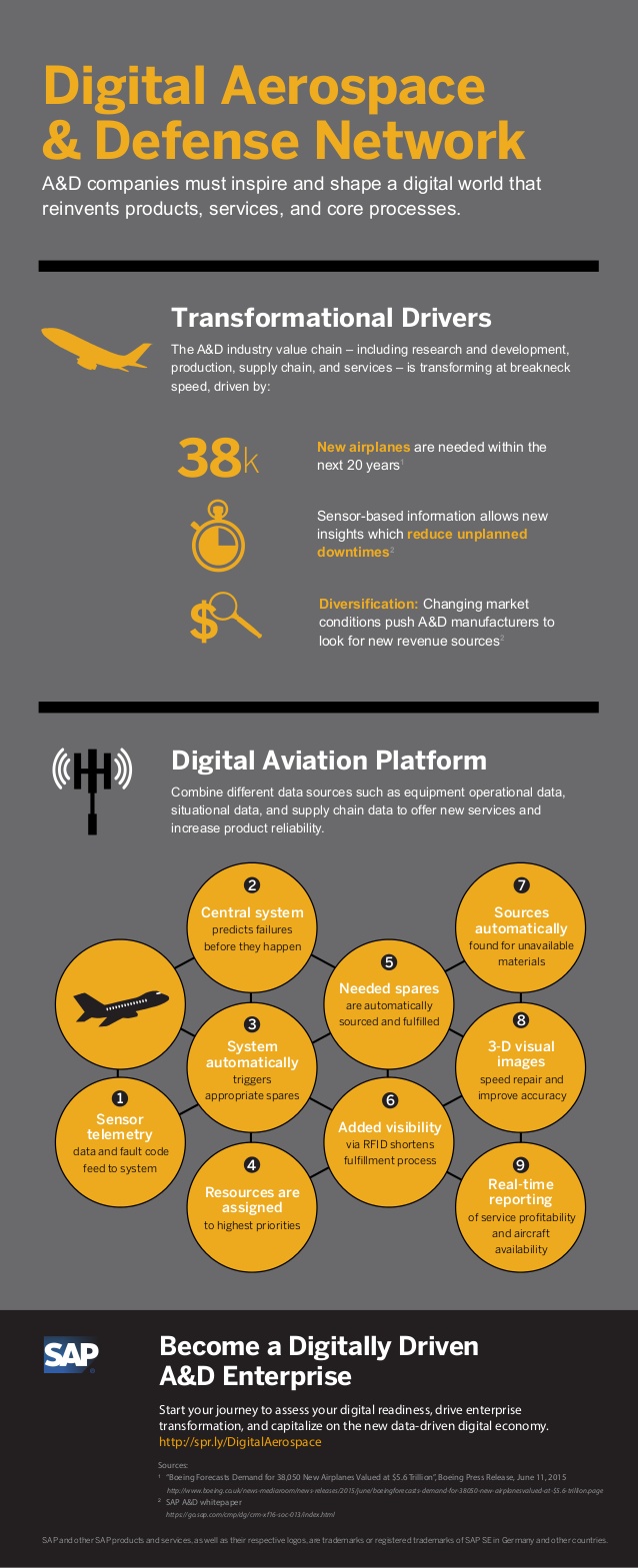

The aerospace and defense [A&D] industry is in a situation that can only be described as challenging. In most nations around the world, the spending on defensive aerospace equipment as been placed under intensive pressure. Because of this, many governments have shifted funding away from defensive programs to other needs.

According to StrategyAnd, defense companies spend far less on R&D (2.2% of revenues on average) than do most U.S. technology companies – 7.6% of revenues on average.

Because there has been a shift to developing more lower-cost digital solutions for key aerospace and defense needs, the call has gone out to many in this industry to invest more into research and development. Yet with direct competition from non-defense companies, such as Apple, Google, and Microsoft, that may not be the only trend that needs to be focused upon today and in the years to come.

Slow and Steady Growth Can Still be Achieved

- According to Deloitte Global, the worldwide aerospace and defense industry is expected to return to growth in 2016 with total sector revenues estimated to grow at 3%.

- This positive signal follows years of declining revenue growth of 3.2% in 2013 and 1.9% growth in 2014. An expected decline of 0.5% in 2015 cannot be confirmed to a lack of released data at the time of this writing.

- Over the last 3 years, global A&D industry revenue was largely impacted by decreased revenues in the United States defense subsector. The anticipated 3% growth for 2016 is based solely on the increase of the US defense budget and a resurgence of global security threats.

- Lower crude oil and other commodity prices, and continued increases in passenger travel demand are contributing to expected growth in production rates for next-generation commercial aircraft.

- As governments equip their armed forces with modern defense weapons platforms and next-generation technologies, including cyber, intelligence gathering, defense electronics, and precision strike capabilities, additional growth opportunities are expected for the A&D industry.

- There are currently about 1.5 million people who are in the air on a plane at any one time on the planet right now, yet only 5% of the world’s population reports being on an airplane.

- The Boeing 747 consists of 6 million parts, which offers additional development opportunities along the industry chain.

- With firm support from governments, which are the core customers of the A&D industry, a history of engineering prowess, and a reliable cash flow, look for larger companies to pick up smaller ones through the M&A process in the next 5 years so fast mobilization on projects can occur once they are approved.

The United States is the world leader when it comes to aerospace and defense. The combined defensive budget for the US is greater than many of its closest allies combined. It is the one nation that has a global military presence which is maintained on a regular basis. Do you see German airbases on US soil? Of course not. Although this globalization is a throwback to the days after WWII, it is still maintained and will be for the foreseeable future as terrorist threats evolve and wars are threatened. As long as that is happening, this industry will have a good chance of experiencing ongoing profits.

Europe’s A&D and How it Compares Globally

- According to the AeroSpace and Defence Industries Association of Europe, military turnover for all sectors (Aeronautics, Land, Naval, and Space) stands at 97.3 billion euro.

- Aeronautics turnover level represents 140.5 billion euro compared to 138.4billion euro in 2013.

- Space revenues indicate a significant growth of 7.5%.

- Civil Aeronautics showed an increase of 2.6% with a turnover amounting to 91.6 billion euro.

- Total exports, both intra-Europe and outside of Europe show an amount of 109 billion euro being spend. Out of this total figure, 68 billion euro represent exports outside of Europe and 41 billion euro as intra-Europe.

- 51.3% of the spending for the A&D industry in Europe is for civil matters, providing a turnover within the industry of 199.4 billion euro in total. That’s an increase of 1%, which helps to offset the expected 0.5% inflation anticipated in coming years that will create a net decrease of $1 billion annually in revenues.

- Aeronautics accounts for two-thirds of A&D spending which occurs in Europe.

Although the overall spending in Europe as a continent is only about 33% of what total US spending happens to be, the trends on the continent are growing in a similar fashion as they are across the pond. Employment is up 2.2% in the A&D sector in Europe, with a heavy focus on creating aeronautic technologies. The US may have Boeing, but Europe has Airbus, and this creates some global competition for sales. The bottom line is this: many Western civilizations are feeling threatened today with the actions of nations like North Korea or independent groups attacking soft targets. The spending trends are going to continue as long as these threats exist.

How to Get Past the Era of Big Weapons

- Outside of R&D investments, the A&D industry can benefit from being able to navigate the halls of military and political headquarters to communicate in a language the funding parties understand. New businesses or those with less experienced technology enterprises could be at a disadvantage when it comes to direct communication.

- To generate immediate incomes, look for some in the industry to become more inclined to sell off-the-shelf commercial products to the Pentagon than to tolerate the lead times, delays, intellectual property rules, and elbow rubbing that are typical of a long-term defense contract.

- Partnering with Silicon Valley can help A&D contractors begin to develop or enhance defense equipment and systems with improved performance and capacities to maintain revenue levels.

- A&D companies can branch out even further into new military sectors that are driven by information technology but are just new theaters for traditional conflicts: cyber defense, for example.

- Look for the industry to also begin a push to retrofit existing weapons platforms with additional offensive and defensive capabilities as A&D technologies continue to evolve.

The problem which the aerospace and defense industry faces right now in an era when bigger weapons aren’t seeing orders is clarity. As administrations change or defensive needs evolve, the needs to address new theaters of conflict will not always be communicated to the industry as a whole. Only those who know how to navigate the existing channels of communication are going to be able to find the funding necessary for these new projects – but even then, they’ll need to patient for the funding to come through, if it ever does.

Global Success Depends on Regional and Local Issues

- In global terms, the annual military expenditures from all nations are expected to exceed $1.7 trillion in 2016, according to Statista, and continue growing in the years to come.

- The change of military spending in North Africa between 2005-2014 was 148% for all parties involved.

- At 13.7%, Saudia Arabia has the highest military expenditure as a percentage of their GDP, yet at $600+ billion annually, the US has the highest military spending worldwide.

- By 2026, Statista expects US defense spending to exceed $719 billion. This means every person in the United States pays $1,864 in order to support the aerospace and defense industry through taxes.

- The US market share of leading exporters of major weapons is 33%. In comparison, India’s share of imports of major weapons is 14%.

- Between the arms sales of Lockheed Martin and the defense, aerospace, and security revenues of Boeing, the two companies are responsible for $67 billion in value for the A&D industry annually. Northrop Grumman contributes another $23 billion in revenues for the industry.

- Lockheed and Boeing also have agreements with NASA that equal 3-4% of their annual revenue, including the space exploration, satellite launching, rocket development, and other similar programs.

- Local tax breaks and other tax laws affect the success of these companies, which then affects the global industry because of the size of the US industry. A $10 million tax break in February 2016 offered by the city of Gresham is just one example of how local issues can affect global success.

From a US perspective, the need for higher defensive budgets is almost a necessity. With attacks in Nice, Paris, Brussels, Orlando, and San Bernadino all attributed to global political and/or religious terrorism in the past 18 months, many US citizens are feeling uneasy. They’re willing to spend a little more to provide an increased security presence around the world so they can feel safe at home. The A&D industry will benefit from this in the coming years, but this does not eliminate the need to be able to innovate within the industry. Those who innovate will dominate. Those who do not will be waiting to pick up the scraps which may or may not receive funding.

Although millions of people visit Brandon's blog each month, his path to success was not easy. Go here to read his incredible story, "From Disabled and $500k in Debt to a Pro Blogger with 5 Million Monthly Visitors." If you want to send Brandon a quick message, then visit his contact page here. Brandon is currently the CEO of Aided.