Compound Interest: Effects On Savings, Emergencies And Retirement

When planning for the future, whether it includes preparing for emergencies, planning for retirement or both the only thing that is certain is a solid plan can provide a clear path toward reaching your goal.

Putting together a plan should always include a variety of factors. An important reality to consider is how compound interest will affect your plan. Compound interest can completely derail your plan or it can make life easier. When assessing compound interest understand that it can have one of two results, positive or negative.

Negative Effects to Compound Interest

Let’s analyze the detrimental effects of compound interest.

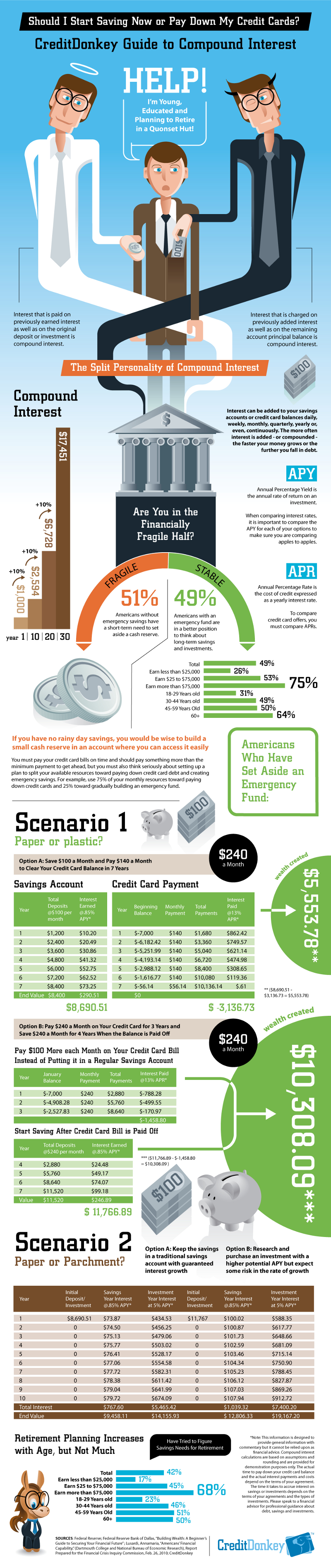

Here is sobering statistic 51% of American do not have a concise emergency savings plan. When life does not present anomalies and you are relatively young, reserved funds may seem irrelevant. However as an individual approaches retirement age or is faced with an unexpected calamity requiring capital sleepless nights and an anxiety driven outlook can dominate your life.

Financially Planning for the Future

Individuals who implement a plan and make the necessary sacrifices in preparation for anomalies or retirement generally fare better.

The 49% of Americans who have an emergency savings plan are broken down here:

• 26% of individuals who earn less than $25,000.

• 53% who earn between 25k-75k.

• 75% who earn more than 75k.

• 31% of 18-29 year old.

• 49% of 30-44 years old.

• 50% of 45-59 years old.

• 64% of 60+ years old.

This list represents individuals who have created a safety net for themselves and their family. Many plans can be created to combat the lack of reserved funds. This article will present a strategy that can be used by anyone without a plan or by individuals who aren’t confident in the plan they have.

Eliminating Debt

Let’s tackle this issue by addressing the issue that plagues most Americans, eliminating credit card debt.

Of course it’s common knowledge that we should pay our credit card bills on time. But credit card debt should not be approached with a narrow view. When interest is factored the credit landscape changes significantly. Making the minimum payment is not enough and can result in a never ending payment cycle.

If you only pay on the principle you are doing very little to affect the bottom line because interest on credit card debt can accumulate daily, monthly or annually resulting in negative compound interest. The best approach to credit card debt is to grapple with the total balance aggressively. If you don’t you will inevitably lose (barring winning the lottery).

Form a Plan

Forming a plan that works is the first step in the right direction. The second step represents consistently sticking to step one. Let’s explore two scenarios to help you meet your goals. Let’s simply identify them as scenario 1 and scenario 2. Scenario 1 will have two parts we will identify as option A and option B.

Scenario 1

With scenario 1 (option A) we will apply a specified amount of monthly funds toward paying down credit card debt and a portion deposited in a savings account.

All things considered let’s assume that $240 is the committed amount to allocate monthly for a period of 7 years. Before we identify the results of a 7 year plan let’s identify two industry terms used by when interest is a calculated.

Interest earned on a savings account is termed Annual Percentage Yield (APY). Interest charged on a credit card account is termed Annual Percentage Rate (APR).The sample plan we will present will set the APY at .85% for traditional savings accounts and 5% for high interest investment accounts. The APR we will set for credit card debt is 13%.

Let’s assume your total credit card debt is $7,000 and the total monthly payment we will divide between the savings account and credit card account is $240. We will deposit $100 in savings monthly and $140 monthly toward the credit card balance.

FYI – the general rule when structuring a plan like this is to allocate 75% toward debt and 25% toward savings emergency fund.

Back to our example, scenario 1 option A.

Assuming scenario 1 (option A) is implemented and not deviated from during the 7 year period the account holder will accumulate $8,400 in savings and gain $290.51 in interest @.85 APY at the end of the 7 year term. The total gained in savings will be $8,690.51. Hence positive compound interest.

Simultaneously you will pay $140 per month toward credit card debt. Again, for purposes of the example the credit card debt is set at $7,000. Seven (7) years of punctual monthly payments of $140 @13% APR will reduce the credit card balance from $7,000 to $56.14. The final payment of $56.14 in year 7 will result in an effective $0 balance and the elimination of credit debt.

Keep in mind that during the 7 year period you were charged a total interest of $3,136.73 (@ 13% APR) against the $7,000. Assuming the credit card interest will be paid from the money gained in savings emergency account ($8,690.51). The result will be $8,690.51 – $3,136.73 with a grand total of $5,553.78 saved. That’s an extra $5,500+ you didn’t have when you started the plan in year 1.

Now let’s review scenario 1 option B. The APR and APY are the same and the plan will also occur within a 7 year period. However option B will produce greater savings compared to option A. Let’s examine the outcome.

With this plan we will pay $240 per month toward the credit debt exclusively for 3 years. After the debt is eliminated we will deposit $240 per month for 4 consecutive years into the savings account. Paying $240 per month for 3 years will produce a $0 credit balance. The total interest charged to you will be $1,458.80 @13% APR. After 3 years has commenced phase II (of option B) will start. Depositing $240 into the savings/emergency account during years 4-7. This will result in $11,520 accumulated in savings.

Interest gained @.85% APY over the 4 year period will result in $246.89 accrued. Assuming funds from the savings account will be applied to the interest charged from the credit card debt ($1,458.80). Total savings will be $10,308.09 ($11,520 – $1,458.80) after the 7 year period.

The result is $10,000+ extra dollars saved that you didn’t have in year 1 of the plan with the elimination of all credit card debt.

Scenario 2

Scenario 2 presents a plan to grow your savings in a high bearing interest account. This plan presents greater financial rewards but has a higher risk. It is important to conduct concise market research or to employ a financial specialist to assist you with minimizing risk when choosing an investment account.

Scenario 2 is a continuation of savings after the initial 7 year period has been successfully completed. Scenario 2 is a 10 year savings plan. We will analyze the results of continuing to save in a traditional low bearing interest account @.85% APY. Compared to saving in a high interest bearing account @5% APY.

After depositing the entire amount saved in scenario 1 option A and letting it accrue for 10 years @.85% APY, $767.60 in interest will be gained. Totaling $9,458.11 (8,690.51 + 767.60). If the same amount is deposited from scenario 1 option A into a high interest investment account @5% APY the results are significantly different. Over a 10 year period $5,465.42 of interest will be accrued with a grand total of $14,155.94 gained (8,690.51 + 5,465.42).

If we deposit savings earned in scenario 1 option B ($11,767) into a traditional savings account @.85% APY the results is $1,039.32 interest accrued in 10 years with a total gain of $12.806.33. Depositing the same amount ($11,767) in a high interest investment account @5% APY results in $7,400.20 interest accrued and $19,167.20 total gained ($7,400.20 + $11,767).

Statistics of Planned Retirement

Continuing with the theme of planning for the future let’s analyze a relevant statistic. Americans who plan for retirement make up B of the population.

The following stats further breaks down the 42% of individuals who prepare for retirement:

• 17% of Americans who make less than 25,000.

• 45% who earn between 25k-75k.

• 68% who earn more than 75k.

• 23% of 18-29 years old.

• 46% 30-44 years old.

• 51% 45-59 years old.

• 50% older than 60.

In essence it’s never too late to plan for retirement. But delaying to plan for the future can necessitate working later in life or relying on public assistance (which isn’t guaranteed). When it comes to preparing for emergencies or the future the proverb “failing to plan, is planning to fail” can be a harsh reality.

Although millions of people visit Brandon's blog each month, his path to success was not easy. Go here to read his incredible story, "From Disabled and $500k in Debt to a Pro Blogger with 5 Million Monthly Visitors." If you want to send Brandon a quick message, then visit his contact page here.